What is balance reformation in 1s. Accounting info. Preparatory stage of the reformation

The last entries that the accountant makes at the end of the year in the sales, other income and expenses and profit accounts are the balance sheet reform entries. We will explain in our consultation what the balance sheet reformation, which is carried out on December 31 of each year, consists of.

Step 1: close account 90

Let us remind you that the following sub-accounts are usually opened for account 90 “Sales” (Order of the Ministry of Finance dated October 31, 2000 No. 94n):

- 90-1 “Revenue”;

- 90-2 “Cost of sales”;

- 90-3 “Value added tax”;

- 90-9 “Profit / loss from sales.”

Synthetic account 90 (“collapsed”) is closed monthly and has no balance at the end of the month. However, during the year, debit or credit balances accumulate in subaccounts to account 90, depending on the type of subaccount. So, since revenue is reflected, for example, in accounting entry D 62 - K 90-1, a credit balance accumulates in subaccount 90-1 during the year. And due to the fact that the cost of sales is written off, for example, by posting D 90-2 - K 43, subaccount 90-2 has a debit balance on each reporting date during the year.

And only on December 31, subaccounts to account 90 are closed: subaccounts 90-2, 90-3, etc. closed to subaccount 90-9. For example, subaccount 90-2 at the end of the year will be closed like this:

Debit subaccount 90-9 - Credit subaccount 90-2

After all debit balances of subaccounts to account 90 are written off to subaccount 90-9, it is necessary to close subaccount 90-1 to this subaccount 90-9:

Debit of subaccount 90-1 - Credit of subaccount 90-9.

This accounting entry simultaneously resets subaccounts 90-1 and 90-9.

Step 2: close account 91

The following subaccounts are usually opened for account 91 “Other income and expenses”:

- 91-1 “Other income”;

- 91-2 “Other expenses”;

- 91-9 “Balance of other income and expenses.”

Similar to account 90, on account 91, on the credit of subaccount 91-1, a credit balance of income accumulates during the year, and on the debit of subaccount 91-2, a debit balance of expenses. Subaccount 91-9 can have both a credit and a debit balance, depending on whether there were more profits or losses during the year. At the same time, synthetic account 91, like account 90, is closed at the end of each month and has no balance.

At the end of the year, the debit balances of the subaccounts of account 91 are written off to subaccount 91-9:

Debit subaccount 91-9 - Credit subaccount 91-2

And then subaccount 91-1, by analogy with subaccounts for account 90, is closed to subaccount 91-9:

Debit subaccount 91-1 - Credit subaccount 91-9

Step 3: close account 99

Where profits and losses from ordinary activities and other operations are written off monthly during the year, it is also subject to closure at the end of the year. Profit reformation is when, by the final entry of December, account 99 is closed to account 84 “Retained earnings (uncovered loss)” and thereby reset to zero.

If the total profit for all types of activities at the end of the year is:

Debit account 99 - Credit account 84

If the year ends with a loss:

Debit account 84 - Credit account 99.

Balance Reformation: An Example

When using specialized accounting programs, the balance sheet reformation at the end of the year is carried out automatically.

Let us show with an example how to perform the reformation manually.

Let's assume that at the end of the year the following balances were accumulated on accounts 90 and 91:

Let us reflect the closure of subaccounts to accounts 90 and 91:

| Operation | Account debit | Account credit | Amount, rub. |

|---|---|---|---|

| The closure of subaccount 90-2 is reflected | 90-9 | 90-2 | 821 370,92 |

| The closure of subaccount 90-3 is reflected | 90-9 | 90-3 | 207 101,95 |

| The closure of subaccounts 90-9 and 90-1 is reflected | 90-1 | 90-9 | 1 357 668,37 |

| The closure of subaccount 91-2 is reflected | 91-9 | 91-2 | 217 029,01 |

| The closure of subaccounts 91-9 and 91-1 is reflected | 91-1 | 91-9 | 101 367,17 |

We will complete the balance sheet reformation operations with the accounting entry for closing account 99.

Step 1. Closing the period

To identify a loss in the 1C 8.3 Accounting 3.0 program, it is necessary to close the period at the end of the year. Closing a period is performed using the Closing month operation from the Operations item.

What needs to be done before closing the month or year before drawing up any declaration in 1C 8.3, read in

In the operation Calculation of income tax, entries are generated to reflect the loss, as well as reversing amounts of tax accrual for previous periods, if a loss was identified at the end of the year:

Important! If there is a loss, then there is no need to immediately reform the balance sheet.

Step 2. Reflection of amounts for loss transfer

The total amount of the loss can be tracked in the declaration. The loss is reflected in sheet 2 on page 060 Total profit (loss). This amount can be transferred to:

If PBU 18/02 is applied, then it is necessary to control the amount of Deferred Tax Assets (DTA) in account 09:

Step 3. Transfer of losses to deferred expenses

To implement the transfer of losses to deferred expenses, you must manually enter a transaction as of the end of the year: item Transactions – Transactions entered manually.

The document must reflect two entries:

- Dt 97.21 Kt 99.01.1 for the amount of loss (line 060 of the declaration) according to NU and VR, the amount of loss with the sign “-”;

Important! If the organization does not accept PBU 18/02, then the amount is not reflected in the postings.

- Dt 09 Expenses of future periods Kt 09 Losses of past periods in the amount of ONA according to accounting;

Important! This posting is indicated if the organization applies PBU 18/02:

In 1C 8.3, in the settings of deferred expenses, it is necessary to reflect the write-off parameters and the amount of loss:

To control ONA in 1C 8.3, you can again generate a balance sheet for account 09:

Important! If losses are reflected in several previous periods, then the losses are taken into account in their order.

Step 4. Balance Reformation

Important! Before performing this operation in 1C 8.3, you must disable .

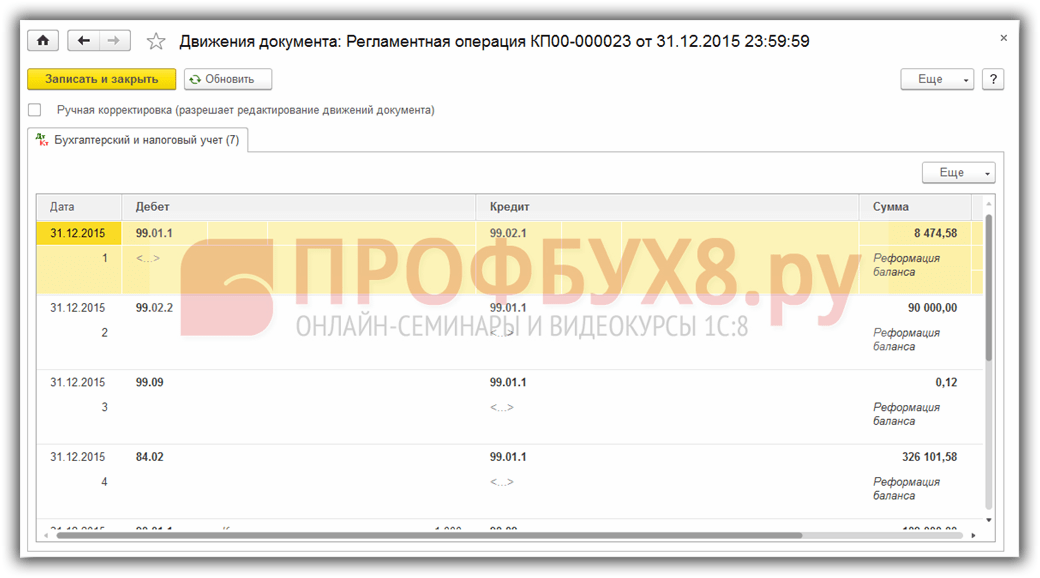

After performing the above manipulations, it is necessary to reform the balance sheet at the end of the period:

Postings are generated:

Step 5. How to write off losses from previous years in 1C 8.3

Until future expenses with the type NL Losses of past periods are not written off when closing the period, the regulatory operation Write-off of losses of past years will be added:

To control the write-off of the amount of loss in the current period in 1C 8.3, a calculation certificate is generated: Write-off of losses of previous years, which can be generated immediately from the Month Closing form using the Calculation certificates command:

If the amount of profit does not allow you to write off the amount of the transferred loss immediately, then the remainder of the amount of the loss from previous periods will be carried forward to the following months until it is completely written off:

Please rate this article:

Closing the year in 1C 8.2 is the final operation before drawing up the annual report. The last entries that you will make for the year are the entries for the reformation of the balance sheet, that is, the closing of the year. This process is automated in 1C 8.2. The program independently makes the necessary records on the reformation. In this article you will learn about closing the year in 1s 8.2 with step-by-step instructions.

Read in the article:

When closing the year in 1C 8.2, you need to perform a number of certain procedures. In particular, reset the balance in accounts 90 “Sales” and 91 “Other income and expenses”. After this, you can begin to reform the balance sheet and record the profit or loss received for the reporting year. These procedures in the program are carried out in 5 steps.

Step 1: Open the Monthly Closing window

Open the “Operations” section (1) and select the “Month Closing” link (2). A special “Month Closing” window will open.

Step 2. Fill in the required fields

In the window that opens, fill out the “Organization” field (3) and indicate the last month of the year being closed, for example “December 2018” (4). In order for the year-end closing procedure to be successful, all previous months, from January to November, must also be closed sequentially in a similar manner.

Step 3. Document verification

To correctly close the year in 1C 8.2, you need to take into account all the operations that were recorded in the program during the year based on primary documents. All documents must be included in the program in chronological order. If you made corrections to the documents, then the accounting entries for them need to be updated. To simplify this procedure, 1C 8.2 has a special link “Control the sequence of documents” (5).

- red – the sequence of documents taken into account in the program is broken;

- green – documents are correctly taken into account in the program.

If the link is red, then in the 1C document program you need to update the accounting records. To do this, click on it. The “Checking the sequence of document processing” window will open. In the window that opens, click the “Repost Documents” button (6):

After the accounting records for the documents are consistently updated by the 1C program, the link “Control the sequence of documents” will turn green (7):

Step 4. Complete year closing in 1C 8.2

To complete the year-end closing operation, click “Perform month-end closing” (8).

1C 8.2 will independently create all the operations that are needed to close December and the year as a whole. Their list is in sections 1 – 4 of the “Month Closing” window. For example, it will write off balances on accounts 20, 23, 25, 26 and 44, and also make the necessary entries on accounts 90 and 91. As a result, all transactions in this window will be colored green. Closing the year in 1C 8.2 is completed. The Monthly Closing window will look like this:

Step 5. Check the closing of the year in 1C 8.2 using the balance sheet

The balance sheet reformation provides for the closure of all subaccounts to accounts 90, 91, 99. As of December 31, there should be no debit or credit balance on them. It is better to check the correctness of closing balance sheet accounts at the end of the year in 1C 8.2 using the balance sheet. At the end of the year, the balance for them should be zero. After closing the year and reforming the balance sheet, the statement may look like this:

Reformation of the balance sheet is the final operation of accounting and tax accounting for the current year. In 1C programs this procedure is automated. However, to reveal its essence, it is necessary to familiarize yourself with the procedure for reflecting information on the formation of financial results and calculations of income tax using PBU 18/02 during the reporting year. These issues are covered by consultants from the 1C:Servistrend company.

First, let's remember what transactions were reflected in accounting and reporting when making income tax calculations. When reflecting in accounting and financial statements calculations of income tax based on the results of the first quarter, half a year, nine months, year, the organization carries out actions recorded by the following changes in accounts (the digital code and names of accounts are given in accordance with the standard setting of the Chart of Accounts in the programs " 1C"):

Debit 90.9 “Profit/loss from sales” Credit 99.1 “Profits and losses” - financial result of the current period (profit received); Debit 91.9 “Balance of other income and expenses” Credit 99.1 “Profits and losses” - financial result of the current period (loss received); Debit 99.1 “Profits and losses” Credit 90.9 “Profit/loss from sales” Debit 99.1 “Profits and losses” Credit 91.9 “Balance of other income and expenses” - monthly advance payments for income tax; Debit 68.4.1 “Calculations with the budget” Credit 51 “Current account” - conditional income tax expense calculated according to accounting data (profit received); Debit 99.2.1 “Conditional income tax expense” Credit 68.4.2 “Calculation of income tax” - conditional income for income tax calculated according to accounting data (loss received); Debit 68.4.2 “Calculation of income tax” Credit 99.2.2 “Conditional income for income tax” - permanent tax assets based on transactions made during the reporting period with positive permanent differences; Debit 99.2.3 “Permanent tax assets and liabilities” Credit 68.4.2 “Calculation of income tax” - permanent tax liabilities based on transactions made during the reporting period with negative permanent differences; Debit 68.4.2 “Calculation of income tax” Credit 99.2.3 “Permanent tax assets and liabilities” - deferred tax assets based on transactions made during the reporting period with deductible temporary differences when accrued; Debit 09 “Deferred tax assets” Credit 68.4.2 “Calculation of income tax” - upon repayment; Debit 68.4.2 “Calculation of income tax” Credit 09 “Deferred tax assets” - when written off; Debit 99.1 “Profits and losses” Credit 09 “Deferred tax assets” - deferred tax liabilities based on transactions made during the reporting period, with taxable temporary differences when accrued; Debit 68.4.2 “Calculation of income tax” Credit 77 “Deferred tax liabilities” - upon repayment; Debit 77 “Deferred tax liabilities” Credit 68.4.2 “Calculation of income tax” - when written off; Debit 77 “Deferred tax liabilities” Credit 99.1 “Profits and losses”.

Deferred tax assets and liabilities are written off upon disposal of the assets (liabilities) with which they were associated.

When moving from one reporting period to another, the amounts of the above indicators change. And for each reporting period, their value is either accrued anew (the amount accrued based on the results of the previous period is reversed in full), or adjusted by additional accrual or reversal of part of the amount, determined as the difference between the values of the indicators accrued based on the results of the reporting and previous periods. As a result of adjusting the conditional income tax expense (income) by reflecting permanent and deferred tax assets and liabilities in the balance sheet, the credit balance of account 68.4.2 “Calculation of income tax” acquires a value equal to the amount of tax calculated from the actual profit of the reporting period , formed in tax accounting registers. This amount is determined in the income tax return and serves as the basis for calculating advance income tax payments transferred to the budget. Thus, the annual indicators of current income tax, deferred tax assets and liabilities are formed in stages (on an accrual basis from the beginning of the year).

A) On the balance sheet

- on line 145 - the balance of deferred tax assets.

- on line 240 - the composition of short-term receivables will also include an overpayment to the budget for income tax;

- on line 470 - the financial result obtained by calculation for the period from the beginning of the year will be included in retained earnings;

- on line 515 - the balance of deferred tax liabilities.

- on line 624 - the debt on taxes and fees will be included, including the debt to the budget for income tax.

B) In the income statement

- on line 140 - profit (loss) before tax, total;

- on line 141 - deferred tax assets;

- on line 142 - deferred tax liabilities;

- on line 150 - current income tax;

- on additional line 151 - written off deferred tax assets and liabilities that change the net profit indicator;

- on line 190 - the amount of the financial result on an accrual basis from the beginning of the reporting year, obtained by calculation (net profit, loss);

- line 200 for reference - permanent tax assets and liabilities.

The state of settlements with the budget at the end of the reporting year is determined as the balance in account 68.4 “Income Tax”. Moreover, in the debit of account 68.4.1 “Settlements with the budget” and the credit of account 68.4.2 “Calculation of income tax” in accounting during the reporting year, the amounts transferred to the budget and accrued income tax are separately accumulated.

Balance sheet reformation occurs in 1C programs when posting the “Month Closing” document dated December 31. In this document, you must check the confirmation box in the “balance sheet reform” position.

To generate operations for closing the month of December, and, consequently, the current year, you must perform the following steps sequentially.

1. Post the document (menu "Documents") "Month Closing" dated December 31 of the reporting year, checking all the boxes except the last four (Fig. 1).

Rice. 1. Closing the month

At this stage, the financial result of the reporting year (profit or loss) is determined, written off from the debit (credit) of accounts 90.9 and 91.9 to the credit (debit) of account 99.1 “Profits and losses”.

2. Post the document (menu “Tax Accounting”) “Routine Operations for Tax Accounting” dated December 31 of the reporting year with all the boxes checked except the last one (Fig. 2).

Rice. 2. Closing the month for tax accounts

After carrying out this document, permanent and temporary differences can be identified between the tax base for income tax and the accounting financial result.

3. Post another document “Month Closing” dated December 31 of the reporting year, checking the boxes only in the positions corresponding to operations according to PBU 18/02 (Fig. 3).

Rice. 3. Closing the month (application of PBU 18/02)

When applying PBU 18/02, deferred and permanent tax assets and liabilities are recognized, repaid and written off, due to which the current income tax formed on the credit of subaccount 68.4.2 acquires a value equal to that calculated in the Income Tax Declaration, that is, in tax accounting .

The above sequence of actions corresponds to the monthly closing operation performed during the reporting year.

4. Post another document “Month Closing” dated December 31 of the reporting year, checking only one checkbox for the “Balance Sheet Reformation” operation (Fig. 4).

Rice. 4. Balance reform

5. Carry out the second document “Routine operations for tax accounting” dated December 31 of the reporting year, also checking only one box for the operation “Closing tax accounting accounts” (Fig. 5).

Rice. 5. Closing tax accounts

Currently, some experts also include the closing of income tax accounts 68.4.1 “Calculation with the budget” and 68.4.2 “Calculation of income tax” as part of the balance sheet reformation process. This operation is carried out manually. To do this, you need to post the document "Accounting certificate" (menu Journals, General documents).

Thus, we entered the last transaction into the journal of business transactions for the reporting year. The balance has been reformed. Tax accounts are closed. Accounting for profits and losses and income taxes will begin in the new year from the beginning, “from scratch.”

Now let’s look at what transactions will be generated by 1C: Accounting automatically when posting the above documents.

1. The amounts of advance payments for income tax made during the year are counted against the payment of current income tax:

Debit 68.4.2 "Calculation of income tax" Credit 68.4.1 "Calculations with the budget."

Depending on the decision made by the organization to close the sub-accounts noted above, the following actions can be performed.

2. The amount of overpayment of income tax can be transferred from the debit of subaccount 68.4.1 to a specially created subaccount of account 68 “overpayment of income tax for previous periods” or included in deferred tax assets:

Debit 09 “Deferred tax assets” (overpayment of tax) Credit 68.4.1 “Calculations with the budget.”

3. The resulting income tax debt is transferred from the credit of account 68.4.2 to the credit of a specially created subaccount of account 68 “Debt to the budget for income tax.”

4. The balance on the subaccounts of account 90 is written off from the credit (debit) of subaccounts 1 to 8 to the credit (debit) of account 90.9 “Profit, loss from sales.”

5. The balance on the subaccounts of account 91 is written off from the credit (debit) of accounts 91.1 “Other income” and 91.2 “Other expenses” to the debit (credit) of account 91.9 “Balance of other income and expenses”.

6. The balance of the subaccounts of account 99 “Profits and losses” is written off from the credit (debit) of accounts 99.2.1 “Conditional income tax expense”, 99.2.2 “Conditional income tax income”, 99.2.3 “Fixed tax assets” and liabilities" to the debit (credit) of subaccount 99.1 "Profits and losses".

How these transactions are reflected in the program, see Figure 6.

Rice. 6. Posting the balance sheet reformation.

7. The balance formed on account 99.1 “Profits and losses”, namely the net profit (loss) of the reporting year, is transferred to account 84 “Retained earnings (uncovered loss)”:

Debit 99.1 Credit 84 - profit made; Debit 84 Credit 99.1 - loss received.

As a result, at the beginning of the new reporting year, subaccounts 68.4.1, 68.4.2, as well as accounts 90, 91, 99 do not have a balance.

At the end of the tax period, the 1C program also closes tax accounts - analogues of accounting accounts in tax accounting.

If an organization receives a loss, then a special procedure for accounting for it, defined by the Tax Code of the Russian Federation, comes into force.

As a general rule, losses are carried forward to the future. That is, the tax base of the current period will not be reduced by the amount of this loss, it will reduce the tax base over the next ten years. And according to the rules of PBU 18/02, a future decrease in the tax base for profit tax and, accordingly, the profit tax itself leads to the formation of a tax asset of the organization (clauses 11, 14 of PBU 18/02).

Let's look at the example of tax accounting for losses.

Example

According to accounting data, a loss was received (-100,000 rubles).

If in the reporting (tax) period an organization incurred a loss, the tax base for profit tax in tax accounting in this period is recognized as equal to zero (clause 8 of Article 274 of the Tax Code of the Russian Federation). Thus, in accounting there is a positive difference between the tax base for income tax and the accounting loss, in our example it is 100,000 rubles.

In tax accounting, the amount of loss is carried forward and reduces the tax base of subsequent reporting (tax) periods by no more than 30%.

In accounting, this operation will not lead to a change in financial results in the future, and, therefore, according to paragraph 11 of PBU 18/02, it will be recognized as a deductible temporary difference (RUB 100,000). Paragraph 14 of PBU 18/02 determines that in the reporting period when deductible temporary differences arise, the organization recognizes a deferred tax asset in its accounting. This is the amount of income tax that should lead to a reduction in income tax accrued and payable to the budget in subsequent reporting periods.

Deferred tax assets are reflected in accounting as non-current assets (subclauses 17, 23 of PBU 18/02).

In our example, a loss of 100,000 rubles. - deductible temporary difference.

Debit 68.4.2 Credit 99.2.2 - 24,000 rubles (100,000 rubles x 24%) - reflects conditional income tax income in accordance with paragraph 20 of PBU 18/02; Debit 09 Credit 68.4.2 - 24,000 rub. (RUB 100,000 x 24%) - a deferred tax asset is reflected.

The balance in account 68.4.2 “Calculation of current income tax” according to accounting data will be equal to zero (24,000 rubles - 24,000 rubles = 0). This corresponds to the amount of income tax reflected in the income tax return, that is, in tax accounting.

Quite often, those who are just beginning to deal with the peculiarities of accounting have difficulties understanding the organization of accounting for 90 accounts and their closure. In this article I will try to explain the structure of 90 accounts and the features of their closure using the example of 1C Accounting 8. Let's start with theory, and then we will look at a practical example.

The following are involved in the formation of the financial result:

90 account "Sales", 91 account "Other income and expenses", 99 "Profits and losses".

Organizations receive the bulk of their profits from the sale of products, goods, works and services (realization financial result). Profit from the sale of products (works, services) is defined as the difference between the proceeds from the sale of products (works, services) in current prices without VAT and excise taxes, export duties and other deductions provided for by the legislation of the Russian Federation, and the costs of its production and sale. The financial result from the sale of products (works, services) is determined by account 90 “Sales”. This account is intended to summarize information about income and expenses associated with the organization’s normal activities, as well as to determine the financial result for them. This account reflects, in particular, revenue and cost:

For finished products, semi-finished products of own production and goods;

Works and services of an industrial and non-industrial nature;

Purchased products (purchased for completion);

Construction, installation, design and survey, geological exploration, research and similar works;

Communication services and transportation of goods and passengers;

Transport, forwarding and loading and unloading operations;

Providing for a fee for temporary use (temporary possession and use) of one’s assets under a lease agreement, provision for a fee of rights arising from patents for inventions, industrial designs and other types of intellectual property, participation in the authorized capital of other organizations (when this is the subject of the organization’s activities ) etc.

In 1C Accounting 8 edition 3.0, the following sub-accounts are opened for account 90:

90.01 "Revenue"

90.01.1 "Revenue from activities with the main tax system"

90.01.2 "Revenue from certain types of activities with a special procedure

taxation"

90.02 "Cost of sales"

90.02.1 "Cost of sales for activities with the main tax system"

90.02.2 "Cost of sales for certain types of activities with a special procedure

taxation"

90.03 "Value added tax"

90.04 "Excise taxes"

90.05 "Export duties"

90.07 "Sale expenses"

90.07.1 "Sale expenses for activities with the main tax system"

90.07.2 "Sale expenses for certain types of activities with a special procedure

taxation"

90.08 "Administrative expenses"

90.08.1 "Administrative expenses for activities with the main system

taxation"

90.08.2 "Administrative expenses for certain types of activities with a special procedure

taxation"

90.09 "Profit / loss from sales"

The amount of revenue from the sale of products, goods, performance of work, provision of services, etc. is reflected in the credit of subaccount 90.01 “Revenue” and the debit of account 62 “Settlements with buyers and customers”. At the same time, the cost of sold products, goods, works, services, etc. is written off from the credit of accounts: 43 “Finished products”, 41 “Goods”, 44 “Sales expenses”, 20 “Main production”, etc. to the debit of subaccount 90.02 “Cost sales". The amounts of VAT and excise taxes accrued on products sold (goods, works, services) are reflected in the debit of subaccounts 90.03 “Value Added Tax” and 90.04 “Excise Taxes” and the credit of account 68 “Calculations for taxes and fees”. Subaccount 90.09 “Profit (loss) from sales” is intended to identify the financial result from sales for the reporting month. Entries for subaccounts 90.01, 90.02, 90.03, 90.04, 90.05, 90.07, 90.08 are made cumulatively during the reporting year. By monthly comparison of the total debit turnover on subaccounts 90.02, 90.03, 90.04, 90.05, 90.07, 90.08 and credit turnover on subaccount 90.01, the financial result from sales for the reporting month is determined. The identified profit or loss is written off monthly with final entries from subaccount 90.09 to account 99 “Profits and losses”. Thus, synthetic account 90 “Sales” is closed monthly and has no balance at the reporting date. At the end of the reporting year, all subaccounts opened to account 90 “Sales” (except for subaccount 90.09) are closed with internal entries to subaccount 90-9 “Profit (loss) from sales.”

To summarize information about operating and non-operating income and expenses, account 91 “Other income and expenses” is used.

In 1C Accounting 8 edition 3.0, the following sub-accounts are opened for account 91:

91.01 "Other income"

91.02 "Other expenses"

91.09 "Balance of other income and expenses"

Subaccount 91.01 “Other income” takes into account receipts of assets recognized as other income (except for extraordinary ones). Subaccount 91.02 “Other expenses” takes into account operating and non-operating expenses recognized as other expenses (except for extraordinary ones). Subaccount 91.09 “Balance of other income and expenses” is used to identify the balance of other income and expenses for the reporting month. Entries for subaccounts 91.01 and 91.02 are made cumulatively during the reporting year. The balance of other income and expenses is determined monthly by comparing the debit turnover in subaccount 91.01 and the credit turnover in subaccount 91.02. This balance is written off monthly (with final turnover) from subaccount 91.09 to account 99 “Profits and losses”. Thus, as of the reporting date, account 91 “Other income and expenses” does not have a balance. At the end of the reporting year, subaccounts 91.01 and 91.02 are closed with internal entries to subaccount 91.09.

The composition of operating income and expenses is determined by PBU 9/99 and PBU 10/99. The main part of operating income and expenses consists of income and expenses from the disposal of property (except for the sale of finished products (work, services and goods)) and from participation in other organizations (receipts and expenses associated with the provision for temporary use of the organization’s assets, rights, arising from patents for inventions, industrial designs and other types of intellectual property, income and expenses associated with participation in the authorized capital of other organizations, profit or loss from participation in joint activities).

When depreciable property is disposed of due to sale, write-off due to the end of its useful life and for other reasons, gratuitous transfer, the amount of depreciation of fixed assets and intangible assets is written off to the debit of accounts 02 “Depreciation of fixed assets”, 05 “Depreciation of intangible assets” from the loan accounts 01 "Fixed assets" and 04 "Intangible assets". The residual value of fixed assets and intangible assets is written off from the credit of accounts 01 and 04 to the debit of account 91 “Other income and expenses”. All expenses associated with the disposal of depreciable property (including VAT on sold property) are also written off to the debit of account 91. When materials and other non-depreciable property are disposed of due to sale, write-off due to damage, or gratuitous transfer, their value is written off to the debit of account 91. The amount of buyers' debt for the sold property is reflected in the debit of account 62 "Settlements with buyers and customers" and the credit of account 91. When When carrying out transactions on contributions to the authorized capitals of other organizations and on contributions of participants of a simple partnership to the common property of partners in non-monetary means, a difference usually arises between the value of the transferred property and the agreed upon assessment of the contribution. This difference is reflected depending on its value in the credit or debit of account 91 (the excess of the agreed value over the accounting value is reflected in the debit of account 58 “Financial investments” and the credit of account 91; the opposite ratio is in the debit of account 91 and the credit of account 58). Interest received for the provision of an organization's funds for use is recorded in accounting records in the same manner as income from participation in other organizations. Interest paid for the provision of an organization's funds for use is usually written off as a debit to account 91 "Other income and expenses" from the credit of cash accounting accounts.

In accordance with PBU 9/99 and 10/99, non-operating income and expenses are: fines, penalties, penalties for violations of contract terms received and paid;

Assets received and transferred free of charge, including under a gift agreement;

Receipts for compensation and reimbursement of losses caused to the organization;

Profits of previous years identified in the reporting year and losses of previous years recognized in the reporting year;

Amounts of accounts payable, depositors and receivables for which the statute of limitations has expired;

Exchange differences;

The amount of revaluation and depreciation of assets;

Transfer of funds related to charitable activities, expenses for sporting events, recreation, entertainment, cultural and educational events and other similar events;

Other non-operating income and expenses.

To summarize information on the formation of the final financial result of the organization’s activities in the reporting year, account 99 “Profits and losses” is used. The credit of this account reflects income and profits, and the debit shows expenses and losses. Business transactions are reflected on account 99 according to the so-called cumulative principle, that is, on an accrual basis from the beginning of the year. By comparing credit and debit turnover on account 99, the final financial result for the reporting period is determined. The excess of credit turnover over debit is reflected as the credit balance of account 99 and characterizes the amount of profit of the organization, and the excess of debit turnover over credit is recorded as the debit balance of account 99 and characterizes the amount of the organization's loss. The final financial result of the organization is influenced by:

a) financial result from the sale of products (works, services);

b) financial result from the sale of fixed assets, intangible assets, materials and other property (part of operating income and expenses);

c) operating income and expenses (less results from the sale of property);

d) non-operating profits and losses;

e) extraordinary income and expenses.

The difference between these components of profit or loss is that the financial result from the sale of products (works, services) is initially determined by account 90 “Sales”. From account 90, profit or loss from ordinary activities is written off to account 99 “Profits and losses”. The financial result from the sale of property, operating and non-operating income and expenses are initially reflected on account 91 “Other income and expenses”, from which they are then written off monthly to account 99. Extraordinary income and expenses are immediately attributed to account 99 without prior entry to interim accounts in correspondence with accounts for accounting for material assets, settlements with personnel for wages, cash, etc. In addition, the debit of account 99 reflects accrued payments on profit and the amount of tax penalties due in correspondence with account 68 “Calculations for taxes and fees”. Payments for recalculation of income tax are also reflected in accounts 68 and 99. At the end of the reporting year, account 99 “Profits and losses” is closed. With the final entry of December, the amount of net profit is written off from the debit of account 99 to the credit of account 84 “Retained earnings (uncovered loss).” The amount of the loss is written off from the credit of account 99 to the debit of account 84.

Let's look at a specific example:

In January 2017, Organization LLC produced and sold products. SALT for January before performing the operation “Closing accounts 90.91” will look like:

According to Kt account 90.01.1, we had revenue of 100,000, and according to Dt account 90.02.1, the cost of products sold was 10,000, according to Dt account 90.03, the amount of VAT was 15254.24. In account 90 we have a credit balance of 74,745.24.

After carrying out the routine operation “Closing accounts 90.91”, the SALT will take the form:

Account 90 was closed by posting Dt 90.09 Kt 99.01.1 - 74745.76.

As a result, on account 99 we formed a financial result for the month - a profit equal to 74745.76. After performing the regulatory operation “Calculation of income tax”, the SALT will take the form:

According to Dt account 99.01.1, we have accrued profit tax of 14949, and profit after tax (balance on account 99) will be 59796.76.

In February 2017, Organization LLC also produced and sold products, and also sold some of the materials. Before performing the routine operation “Closing accounts 90.91”, the SALT will have the following form:

As we can see, we have transferred the balance from January on account 99 and subaccounts of account 90. In February, we added a debit turnover on account 91.02 - 5000 - this is the cost of materials sold and a credit turnover on account 91.01 - 15000 - this is the proceeds from the sale of materials.

After performing the regulatory operations “Closing accounts 90.91” and “Calculating income tax”, the SALT for February will take the form:

Account 90 was closed by posting Dt 90.09 Kt 99.01.1 - 72457.62. Similarly, 91 accounts are closed Dt 91.09 Kt 99.01.1 - 10000. Profit tax was accrued by posting

Dt 99.01.1 Kt 68.04.1 - 16492.

As a result, the profit for the first two months of the year will be 125,762.38 (Account balance 99.01.1.

Thus, every month (after performing routine operations) synthetic accounts 90 and 91 do not have a balance. On account 99, profit or loss (account balance) is accumulated on an accrual basis. Also, the cumulative total forms the balance for subaccounts 90 and 91.

At the end of the year, before performing the regulatory operation “Balance Reformation”, the SALT for the year will look like:

After performing the operation "Balance Reformation" we get:

As we see, account 99 is closed, the account balance goes to account 84 “Retained earnings (uncovered loss)”. In addition, all subaccounts 90 accounts are closed with transactions between 90.09 and 90.01.1, 90.02.1, 90.03. Subaccounts of account 91 are closed in the same way - with transactions between 91.09 and 91.01, 91.02.

Thus, all subaccounts 90,91,99 accounts have a zero balance. The balance in account 84 carries over to the next year.